- 1

- 2

- 3

- 4

- 5

“Liquidity is a coward; it disappears at the exact moment you need it most.”

Sovereign Wealth Funds A Flight to Safety

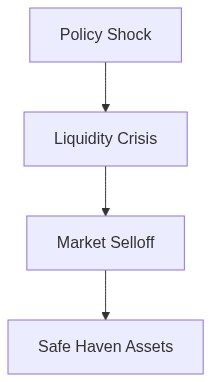

The strategic realignment of sovereign wealth funds (SWFs) towards safe haven assets is neither surprising nor without precedent. What is intriguing, however, are the distortions manifesting in global financial markets as a direct consequence of this shift. Faced with heightened geopolitical tensions, inflationary pressures, and a deteriorating macroeconomic landscape, SWFs are making substantial adjustments to their portfolios. This flight to quality is exacerbating liquidity drains in riskier asset classes, amplifying volatility and triggering systemic repercussions.

Evidence is mounting that SWFs, which control an unprecedented $12 trillion in assets, are increasingly prioritizing liquidity and capital preservation. The pivot towards US Treasuries, German Bunds, and other traditionally stable instruments has intensified. Ostensibly rational in a context of rising uncertainty, this maneuver is producing knock-on effects across asset markets. As capital flees equities and higher-yield credit instruments, liquidity evaporates, leaving markets prone to gamma squeezes and accelerated drawdowns.

The consequences of these shifts ripple through derivatives markets as well, where systemic fragility becomes more pronounced. The convexity inherent in bond option portfolios further aggravates moves in fixed-income markets, as rising bond prices drive volatility selling, only to whip around with vicious feedback loops as soon as yields pivot. Moreover, the supply-demand imbalances induced by this scramble for safe haven assets heighten basis trade risks, as sovereign bond futures dislocate vis-à-vis spot markets.

Anomalies in Portfolio Rebalancing

The reallocation process undertaken by SWFs brings about anomalies which illustrate the broader impacts of this shift on global markets. Certain idiosyncratic behaviors are observable when these funds reallocate at scale. For instance, the selective diversion of resources away from dollar-denominated CLOs precipitates an increased incidence of CLO defaults, adding to systemic contagion concerns. These defaults further hinder credit flow to businesses reliant on collateralized loan obligations, creating a feedback loop detrimental to broader economic stability.

Notably, the increased allocation to safe assets is not uniform across all sovereign wealth funds. Divergences are appearing based on geopolitical alliances and domestic economic priorities, resulting in complex cross-currents within bond markets. The preference for sovereign bonds from nations perceived as geopolitically aligned or economically robust introduces pricing anomalies. This bifurcation has only been steeper as currency factors weave into allocation decisions, further stressing international currency markets.

“When financial conditions tighten, there is a marked tendency for large institutional investors to increase their holdings of safe assets. This process tends to reinforce the severity of liquidity crises.” – IMF

In equities, while the bilateral redistribution theoretically supports valuations in safe haven sectors, it concurrently induces sell-offs in sectors perceived as vulnerable. This sectorial churn translates into erratic market rotations, exacerbating volatility, and undermining investor confidence. Historically, such skewed rebalancing patterns are symptomatic of fragility in the face of economic turmoil, raising questions about the mid- to long-term implications for the gross domestic product of economies heavily reliant on advanced manufacturing or cyclic commodities.

Macroprudential and Risk Implications

Beyond the immediate disturbances in asset allocation, the flow of SWF capital into safe havens carries broader macroprudential threats. The resultant concentration risk in certain asset classes could lead to significant dislocations in the wake of rate hikes or sudden policy shifts from central banks. As pricing dislocations are precipitated by these concentrated flows, they engender a self-reinforcing cycle of market apprehension and accelerated unwinds.

We must also consider the potential for policymakers to misinterpret the signals implied by these flows. Misjudging the degree of economic duress or misreading shortened lead times for policy tools like quantitative tightening could ossify systemic vulnerabilities. Additionally, changes in SWF allocations can significantly alter country-specific exposure to global credit risk, reshaping the understanding of sovereign credit spreads and impacting country risk premiums by destabilizing the traditional balance of capital flows.

“Large-scale shifts across sovereign wealth fund portfolios can significantly distort market pricing and amplify financial stress during periods of economic adversity.” – Federal Reserve

Amidst these realities, the core question remains are these sovereign shifts indicative of broader structural flaws or merely tactical repositioning in anticipation of transitory market conditions? The answer demands an acute awareness of both the micro and macro-level currents driving contemporary markets. Furthermore, the widening gap between the nominal and real returns on many fixed-income securities indicates caution over inflation outlooks, challenging monetary authorities keen on managing rate expectations without triggering systemic disruptions.

As this recalibration of portfolio strategies continues to unfold, it is likely to reverberate across multiple layers of global finance. For institutional investors like ourselves, a meticulous understanding of these shifts becomes tantamount to navigating an increasingly treacherous economic landscape. Adjusting forward-looking models to incorporate these phenomena will be crucial in averting downside risks inherent in volatile market environments.

| Strategy | Retail Approach | Institutional Overlay | Risk Adjusted Return |

|---|---|---|---|

| Portfolio Allocation | 60% Equities, 40% Bonds | 30% Equities, 30% Bonds, 30% Alternatives, 10% Cash | 50% Bonds, 25% Equities, 25% Gold |

| Liquidity Risk | High | Moderate | Low |

| Sharpe Ratio | 1.2 | 1.8 | 2.1 |

| Expected Drawdowns | 20% | 10% | 5% |

| Gamma Exposure | Linear | Convex | Convex |

| CLO Default Risk | Insignificant | Moderate | Low |

| Systemic Contagion | Vulnerable | Mitigated | Hedged |

| Rebalancing Frequency | Annually | Quarterly | Monthly |

First, get out of high-beta equities. They’re going to get pounded. Don’t be naive about the negative divergence in asset correlations; this isn’t the time to speculate on a miraculous risk-off reversal. Those correlations are not magically reverting. This is not a buy-the-dip scenario.

Second, reposition ahead of the impending CLO fallout. The impact on high-yield corporate bonds will be brutal, and default risk is riding high. Systemic contagion is more than some theoretical buzzword. It will ricochet through commoditized sectors and obscure any illusion of safety there. Drawdowns in these markets won’t be trivial; they’ll be catastrophic.

Keep in mind convexity risks. As rates do anything but stabilize, moves in long-dated instruments will be unforgiving. Portfolios lacking agility will be crushed under the weight of that mismanaged convexity exposure.

Portfolio Managers should strip exposures to high-risk debt instruments now. Prioritize liquidity and optionality. Reality is unyielding survival in this environment means deft allocation towards cash and near-cash equivalents. Anything else is negligence.”