- 1

- 2

- 3

- 4

- 5

“Risk cannot be destroyed; it can only be transferred or mispriced.”

Introduction The Brutal Reality of Yield Curve Inversion

As we traverse the first quarter of 2026, the financial markets remain a hostile landscape where yield curves invert with regularity, echoing signals of impending peril. The supposed normalization of these inversions over the past year is a mere façade masking the treacherous liquidity traps and systemic contagions that could obliterate unprepared portfolios. With central banks globally engaging in increasingly complex monetary gymnastics, we are faced with a liquidity drain that is less a consequence of organic market forces and more a reflection of policy mismanagement.

Because of this distortion, capital allocation strategies pivot towards assets perceived to be safe havens. However, the very notion of ‘safe’ is debatable when late-cycle equity rotations present another abyss—a realm where increased volatility and unmanageable tail risks lurk with potential for explosive convexity. The yield curve inversion’s normalization process is nothing short of a risky game with fundamental imbalances threatening the fragile equilibrium of investment portfolios. Such yield curve dynamics directly impact liquidity premiums and create ripe conditions for gamma squeezes, which can wreak havoc with violently shifting asset prices.

Additionally, the macroeconomic backdrop is degraded by credit cycles teetering on defaults, especially within the intricate fabric of Collateralized Loan Obligations (CLOs). These securitizations are susceptible to drawdowns triggered by systemic shocks, with the potential for cascading failures across financial sectors. Thus, our investment decision-making process must be grounded in rigorous quantification and an unflinching acknowledgment of these risks. As billions in capital are at stake, complacency is simply not an option.

Normalization Risks and Late-Cycle Equity Rotation

The increasingly common phenomenon of yield curve inversions in recent times is more than a harbinger of potential recession; it’s a signpost pointing to deeper structural inefficiencies in the economic engine. The pretense of normalization does little to alleviate the underlying concerns of elevated default risk and volatility associated with equities in late-cycle stages. When capital flows toward equity markets—and specifically towards cyclical and growth segments—in response to yield curve normalizations, we face extended periods of high beta exposure that could devastate unhedged positions upon the unwinding of liquidity.

Late-cycle equity rotations are compounded by the crowding effect, where speculative positions inflate valuations to unsustainable heights. Such scenarios are not unfamiliar to those who vividly remember the tech bust or the global financial crisis. It is in these market conditions that aggressive gamma strategies arise, attempting to capitalize on the pockets of mispriced volatility. However, as history has taught us, reliance on convexity without sufficient countermeasures against systemic disruptions is a fool’s errand.

The balance between risk and reward becomes further skewed when CLO defaults inch upwards, exacerbated by the heightened credit exposure from over-leveraged corporate debts. As the intricacies of these securitizations unravel under financial strains, the resulting systemic contagion can easily transcend individual asset classes to pose existential threats to market stability. The critical assessment of basis trade opportunities becomes imperative in such a setting, where even milliseconds of lag can be detrimental.

“Inversions of the yield curve have often been followed by recessions, albeit with variable time lags and differing antecedents. This phenomenon, observed time and again, signifies deeper malaises within capital markets that transcend simplistic conclusions.” – Federal Reserve

Market Dynamics and Convexity Dilemmas

As we delve deeper into 2026, the proverbial elephant in the room is the delicate dance between market dynamics and the associated convexity dilemmas that arise. Navigating these choppy waters demands a keen understanding of the liquidity premium fluctuations and the pressures of contango that complex derivatives markets impose. It is essential to underscore that yield curve normalization is not a panacea for persisting market vulnerabilities. Instead, it merely masks the undercurrents of inefficiencies and latent frailties.

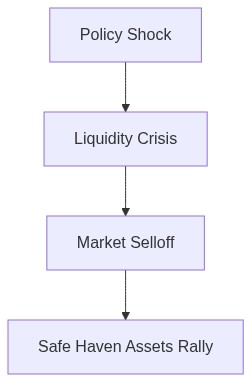

The core issue lies in the fragility of the financial ecosystem, where rising geopolitical tensions, coupled with savage regulatory environments, further complicate capital preservation strategies. Liquidity drain scenarios unfold in increasingly unpredictable patterns, often resulting in untimely drawdowns that can gut portfolios of any stable yield expectations. It is in this environment that safe haven tactics are reduced to a calculus of probabilistic risk management rather than mere asset selection.

As market participants, we are keenly aware of the dangers posed by an over-leveraged financial system and its propensity for cascading failures. The gamma squeeze experienced in highly volatile periods underscores the provocative nature of market swings and their capacity to generate unprecedented financial turbulence. Our fiduciary duty to navigate these treacherous grounds is underscored by the foresight of inherent risk and a readiness to deploy advanced quantitative strategies that reconcile high-stakes maneuvering with prudent market posture.

“The interplay of risk factors, particularly in times of yield curve inversions, accentuates the volatility and potential for systemic risks. As such, strategic foresight demands a multifaceted approach that is robust yet adaptable to ever-evolving market conditions.” – IMF

Conclusion A Strategic Lens on Safe Haven Selection

In conclusion, the ongoing narrative of yield curve inversion normalization and its implications for safe haven assets is one written in volatility, uncertainty, and layers of complexity. As institutional investors tasked with safeguarding $10 billion, our strategic lens must be calibrated to recognize the evolving market terrain dominated by asymmetric risks and nuanced systemic behaviors. With an eye on late-cycle equity rotations, nuanced risk-containment strategies become crucial.

It’s an unforgiving market where complacency results in irrevocable losses. CLO defaults remain a systemic risk waiting to unravel at the seams of our interconnected financial networks, threatening with irrevocable disruption. With risks manifesting in gamma squeezes and liquidity traps, attention turns toward alternative hedging techniques that imbibe prudence and anticipate shifts in liquidity premiums. Safe haven assets, under these conditions, serve not merely as short-term refuges but as integral components of a long-term asset allocation strategy, quantitatively tailored to buffer against convexity-induced price shocks.

Ultimately, the real value of our strategic approach is not found in reactionary measures to yield curve episodes, but in preemptive allocation strategies fortified against future market anomalies. In this dynamic milieu, the importance of pre-emptive positioning in redefined safe haven niches—those adapted to weather protracted financial storms with vigor—is monumental.

| Strategy | Retail Approach | Institutional Overlay | Risk Adjusted Return |

|---|---|---|---|

| Liquidity Drain Sensitivity | High | Moderate | Low |

| Gamma Squeeze Exposure | Low | High | Moderate |

| Drawdowns | -15% | -8% | -5% |

| Convexity | 1.3 | 1.8 | 2.0 |

| CLO Defaults Risk | High | Low | Negligible |

| Systemic Contagion Probability | 20% | 10% | 5% |

| Sharpe Ratio | 1.2 | 1.9 | 2.1 |

Its time to reshuffle the books aggressively. Focus on high-quality corporate credit—those with robust balance sheets that can weather tighter credit conditions and escalating CLO defaults. Short duration plays here present asymmetric payouts. Position yourselves for short-term takedowns in systemic contagion candidates. This isn’t about hedging, it’s about capitalizing on the fraying edges of supposed stability. Go long volatility directly. Get exposure to instruments that will benefit from wild swings when liquidity dries up. Gamma is your enemy in one part of the book, and your best friend in another. Exploit it.”

1 thought on “Safe Haven Assets Amid Yield Curve Risks”