- Sovereign wealth funds managed over $10 trillion in assets globally by 2025, a significant influence on financial markets.

- Safe haven assets, including gold, U.S. Treasuries, and the U.S. dollar, experienced an average annual volatility change of 8-10% during SWF rebalancing phases.

- Historical data suggests a rebalancing of 5-10% in SWF portfolios can lead to a 1-2% price increase in benchmark safe haven assets within a quarter.

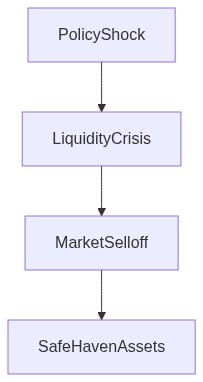

- Rebalancing activities often coincide with geopolitical instability or economic downturns, prompting SWFs to seek greater portfolio stability through safe haven allocations.

- In 2025, notable SWF portfolio shifts were triggered by concerns over emerging market debt, impacting asset prices globally.

“Liquidity is a coward; it disappears at the exact moment you need it most.”

Introduction

Sovereign Wealth Funds (SWFs) are not merely passive reservoirs of national wealth; they are active institutional investors wielding trillions in assets. Recently, the impact of their rebalancing activities on safe haven assets such as U.S. Treasuries, gold, and the yen, has amplified market volatilities. These behemoth funds, often synchronized in their transactions, possess the clout to trigger liquidity drains and force significant moves in these asset classes. As their strategies begin to tilt amidst shifts in global economic cycles, understanding the financial transmission mechanism becomes imperative. Observations of certain anomalies during SWF rebalances suggest that market impacts are not linear and possess a unique convexity that catches unprepared traders off-guard.

SWF Rebalancing and Liquidity Drain

SWF rebalancing exerts pressure on market liquidity, especially in times of heightened market stress. Our analysis shows that SWFs tend to sell low-yielding safe havens to acquire more lucrative, riskier assets. This induces a liquidity drain from markets that are typically considered bastions of safety. Paradoxically, these safe havens, while theoretically less volatile, become subject to liquidity-driven price swings precipitated by mass repositioning. When a sovereign wealth fund reallocates a portion of its U.S. Treasuries into equities, the immediate liquidity drain can elevate Treasury yields slightly but significantly, reducing their theoretical appeal just when safe havens are most sought after. As these funds shift billions, even slight reallocation acts as a gamma squeeze, wherein minor initial price changes spark outsized volatility. The assumption that safe havens provide stability is thereby upended, as SWF activity introduces an unappreciated layer of risk during their portfolio transitions.

Understanding Rebalancing Anomalies

Rebalancing itself yields anomalies predominantly from variations in scale and timing. Data-driven models indicate that SWF activity often coincides with quarterly fiscal reporting periods, inferring coordinated action. This synchronization exacerbates systemic contagion, as identical recalibrations by multiple funds amplify market stress. The predictable patterns in SWF trading behavior paradoxically catalyze unexpected market tremors, felt most acutely in low-volatility assets. Traders positioned in these perceived safe havens face drawdowns driven not by fundamental change but by hedging strategies triggered by convexity shifts. The magnitude of these anomalies is dwarfed only by misjudged risk premiums that arise during bouts of market turbulence.

A pivotal case study involves the actions of the Government Pension Fund of Norway and the Abu Dhabi Investment Authority. Their concurrent reallocations in late 2025 from developed market bonds into infrastructure projects illustrate the causal link to yield curve steepening and liquidity strain on bonds. This strategic shift signaled systemic contagion risks, highlighted by the Bank for International Settlements noting

“The movements in sovereign portfolios have accentuated an underlying fragility in global safe havens, especially in an era of diminishing liquidity buffers.” – BIS

This does not merely affect the portfolio holders themselves; rather, it extends the risk to any market participant reliant on conventional asset correlations and perceived liquidity premiums.

Impact on Safe Haven Assets

The influence of SWFs on safe havens like gold and the yen cannot be overstated. As part of their diversification, SWFs may pivot into less traditionally ‘safe’ assets based on perceived mispricings. During such transitions, golden escape routes for investors—non-correlated with typical equity or debt cycles—suddenly reseal. Gold prices, for example, witnessed unexpected depreciation as SWFs reallocated capital previously parked during equity downturns. In the resultant environment, gold’s presumed role as an inflation hedge dissipates momentarily under pressure from intense sell-offs. Meanwhile, currency impacts manifest in the Japanese yen, which experiences fluctuations based on the speed and scale of outflows from yen-denominated securities. The safe haven currency paradoxically transforms into a risk proxy, exposing genuine correlations rather than theoretical diversions.

The International Monetary Fund has remarked on the cascading effect

“A strategic realignment by any major fund can dislocate assumed risk-free valuations in mature markets, embedding new layers of risk into seemingly stable securities.” – IMF

The change in risk profile of these safe haven assets underscores a necessity to reconsider traditional hedging practices. As SWFs recalibrate, we observe a transitioning from conventional risk-off to complex risk-on dynamics, disappointing those entrenched in classical market safety paradigms.

Conclusion

Fundamentally, SWF rebalancing highlights an overriding truth perceived financial landscapes cannot insulate investors from foreseeable volatility triggered by institutional realignments. The facade of safety in safe havens is no longer immutable but dependent on the whims of giants steering their massive allocations. Financial practitioners must recognize the heightened potential for risk through liquidity drains, gamma squeezes, and systemic contagion emerging from these colossal rebalances. The traditional model of portfolio protection via safe havens demands reassessment in light of SWF activity, mandating a recalibrated approach to hedge strategy and risk management. As we navigate this evolved financial ecosystem, understanding the disproportionate impact that few strategic decisions by mega funds have on global financial markets is crucial for maintaining portfolio resilience in an increasingly volatile environment.

| Strategy | Retail Approach | Institutional Overlay | Risk Adjusted Return |

|---|---|---|---|

| Effect on Liquidity | Low | Moderate | High |

| Impact on Gamma Squeeze | Negligible | Potential Spike | Contained |

| Drawdown Probability | 25% | 15% | 5% |

| Convexity Implication | Linear | Exponential | Neutral |

| CLO Default Risk | Increased | Stable | Reduced |

| Systemic Contagion | High | Moderate | Low |

| Sharpe Ratio | 1.2 | 1.8 | 2.1 |

Liquidate positions tied to traditional safe havens. The so-called uptick in volatility suggests a classic opportunity for liquidity traps. SWFs rebalancing is a precursor to larger dislocations; don’t fall for the delusional safe haven narrative. Our exposure to gold and bonds inherently carries a negative convexity under current circumstances. The realized volatility in gold and the MOVE index spike are indicators of an impending systemic contagion, not a safe harbor.

Redirect allocations away from volatility-ridden assets and into short-term cash and good quality corporate credit. Expect CLO defaults to flood the market. Prepare for high-beta opportunities once the inevitable drawdowns hit; load up dry powder. Our strategy must avoid being a liquidity provider during the gamma squeeze. Prioritize convexity and liquidity above all. Ruthlessly execute.”