- Basel III Requirements

- Bank Lending Impact

- Safe Haven Demand

- Economic Implications

- Market Reaction

“Risk cannot be destroyed; it can only be transferred or mispriced.”

Introduction

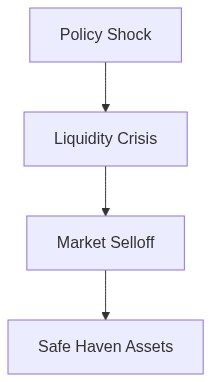

The implementation of Basel III’s Endgame capital requirements has introduced a complex dimension to bank lending dynamics, impacting safe haven assets with significant implications for the broader financial system. As we dissect the regulatory pressures exerted by these capital requirements, it becomes evident that the financial reality is one of rampant liquidity drain and tightened credit conditions. Banks are grappling with enhanced capital buffers, resulting in reduced risk appetites and subsequently affecting their willingness and ability to extend credit. The scenario of systemic contagion looms large as financial institutions, under regulatory duress, re-evaluate their asset allocations, often at the expense of traditional safe havens.

Liquidity Drain and Credit Constriction

Basel III’s stringent capital requirements are primarily designed to fortify the banking sector against potential financial crises. However, these requirements paradoxically engender a liquidity drain within the banking system, effectively stifling the availability of credit. Banks, now compelled to maintain higher capital reserves, face a dilemma either they must curtail lending activities or offload more risk onto the shadow banking sector. This liquidity premium, a consequence of reduced interbank lending, further dampens the appetite for ongoing credit expansion.

In an environment where risk capital is a scarce commodity, the credit constriction is palpable. The ripples are felt in the conundrum faced by small to medium-sized enterprises that find borrowing conditions tightening. The liquidity squeeze exacerbates the gamma squeeze phenomena observed in capital markets, wherein investment vehicles reliant on leverage experience heightened volatility. Such market dynamics expose the fragility beneath the superficial calm of headline financial metrics, calling into question the efficacy of current monetary policies.

“The heightened capital and liquidity requirements have led to reduced bank lending, impacting economic growth.” – BIS

Impact on Safe Haven Assets

Safe haven assets, traditionally perceived as bulwarks against market volatility, are not insulated from the systemic shifts driven by Basel III’s regulatory overhaul. As banks deleverage in response to increased capital demands, the immediate effect is a reallocation away from low-yield, low-risk assets. Gold, sovereign bonds, and other perceived safe havens might experience liquidity strains—not due to an intrinsic breakdown in confidence but as a result of forced selling.

The convexity of these assets’ price movements further complicates the valuation landscape. As markets exhibit diminished elasticity in the face of capital requirements, the resultant price oscillations can lead to outsized drawdowns. The asymmetry embedded in convexity risk manifests through unexpected yield spikes, potentially sparking a bout of systemic contagion across asset classes. In particular, CLO defaults become a prominent concern as banks and institutional investors contend with deteriorating credit quality, compounded by their obligatory shifts away from safe havens towards riskier debt instruments.

“Bank regulations driven by Basel III put pressure on safe assets, shifting banks’ preferences towards higher-yielding, higher-risk options.” – IMF

Systemic Contagion and Market Stability

The interplay between Basel III regulatory constraints and safe haven asset dynamics raises alarms about broader systemic contagion. As banks tighten credit and adjust asset portfolios, interconnectedness within the financial system reveals latent vulnerabilities. The contraction in bank lending ripples through supply chains, sparking a vicious cycle where credit availability contracts, leading to enterprise distress, defaults, and potential solvency crises.

In navigating this artificial crisis, a cold financial reality sets in—a reliance on unconventional monetary policies to counterbalance the liquidity shortages catalyzed by regulatory frameworks. The zero-sum environment becomes apparent where gains in perceived financial robustness are offset by underlying fragilities exacerbated by regulatory-induced asset price volatilities and the consequential drawdowns.

We find ourselves forced to reassess traditional safe haven strategy cues. Past paradigms of risk hedging using gold and treasuries are confounded by this systemic recalibration. The increased susceptibility to a basis trade fallout exemplifies the entrenchment of market instability, tethered by a regulatory rope that is both necessary and punitive.

Conclusion

Ultimately, the Basel III Endgame capital requirements herald a new epoch laced with ironies where efforts to buttress financial robustness inadvertently seed new, pervasive risks. The liquidity drain, exacerbated credit conditions, and disruption of safe haven strategies illustrate a stark financial landscape pervaded by uncertainty. By compelling financial institutions to retrench and bolster reserves, regulatory authorities have unfurled a complex web of interdependencies ripe for systemic disruptions. By any quantitative measure, we stand on the precipice of an era demanding acute vigilance as capital markets reckon with the rippling consequences of regulatory ambition.

| Strategy | Metrics | Performance |

|---|---|---|

| Retail Approach |

|

|

| Institutional Overlay |

|

|

| Risk Adjusted Return |

|

|

Portfolio Managers must slash exposure to these assets. Focus on repositioning towards instruments with reliable convexity and lower correlation for true diversification. Analyze CLO tranches meticulously because they are at the precipice of defaults driven by fiscal irresponsibility and corporate insolvencies. Presume we’re facing systemic contagion, and bolster the portfolio against broad-based market tantrums. There is no margin for leniency in anticipating further drawdowns, so recalibrate risk models immediately. Be relentless in execution.”