- Yen carry trade unwinding causes significant market disruptions.

- Global equities face heightened volatility amid currency shifts.

- Central banks grapple with policy responses to stabilize markets.

- Emerging markets at risk due to capital flow reversals.

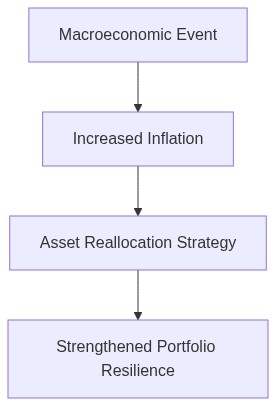

- Inflation hedging strategies need urgent recalibration in volatile climates.

“The market is a mechanism for transferring wealth from the impatient to the prepared.”

The Unprecedented Yen Appreciation Catalysts and Reverberations

The phenomenon of an aggressive Japanese yen appreciation over the past quarter has caught financial analysts off guard, as traditional metrics failed to capture the currency’s meteoric rise. Grounded in both supply-side constraints and robust capital inflows, the yen’s appreciation has unraveled as a multifaceted event. Critical to the upward trajectory has been Japan’s unexpectedly strong macroeconomic data coupled with its advantageous real rate differential. Central to these dynamics is the Bank of Japan’s (BOJ) departure from Yield Curve Control (YCC) to a more normalized rate structure. As the BOJ allowed bond yields to fluctuate more freely, it inadvertently boosted investor appetite for yen-denominated assets, thereby strengthening the yen on FX markets. It is imperative to note that this appreciation has triggered an unwinding of the carry trade, where leveraged positions in low-yield currencies are reversed, often creating unsustainable pressure on the yen.

Equally significant is the balance of trade shift which has underpinned the yen’s appreciation. An uptick in Japanese exports, driven by burgeoning semiconductor and consumer electronics demand, has amassed substantial trade surpluses. This shift is crucially enhanced by Japan’s strategic renegotiation of supply chains, lessening reliance on geopolitical instability-prone regions, thus fortifying its export channels. On parallel planes, global liquidity metrics remain generous, emboldening capital inflows into Japanese assets, reflecting a tactful escape from geopolitical-fraught investment landscapes. This has also been substantiated by non-resident portfolio flows contextually captured in Japan’s outstanding balance of payments data.

Ripple Effects on Global Derivatives Markets A Deep Dive into Volatility Dynamics

The current yen surge has unambiguously radiated implications across global derivatives markets, with convexity and the liquidity premium playing critical roles. In the derivatives sphere, Japanese yen options have undergone heightened implied volatility, symptomatic of participants recalibrating risk profiles. The liquidity constraints exacerbated by the yen’s ascent have injected a premium into these instruments, indicating a recalibration of market resilience. Swaption skews have shifted dramatically, with the yen’s currency options displaying deeply inverted risk reversals – a harbinger of investor hedging against further yen appreciation. Furthermore, interest rate swaps pegged to yen forecasts now reflect a steepening curve, foretasting anticipated volatilities. Such developments point to a profound repricing mechanism unraveling across futures markets tied to yen-denominated assets.

Concomitantly, the derivatives’ world has seen bifurcation, with contango states in particular yen-linked futures markets disrupting valuation narratives. The unexpected yen appreciation has introduced backwardation, deceitfully perceived as a transient state while fundamentally signaling endemic supply-demand imbalances. Treasurers and hedgers alike grapple with shifting risk appetites, epitomized by the challenging recalibration of VAR (Value at Risk) models pivoting toward greater tail-risk sensitivity. Furthermore, market strategies examining delta and gamma are revising assumptions to model the yen’s idiosyncratic movements, establishing complex dynamic hedging portfolios that reflect the resultant non-linear exposures.

Institutional Recalibration Central Bank Strategies and Sovereign Wealth Fund Maneuvers

The sovereign sphere is not impervious to the intrigue surrounding Japan’s yen trajectory; central banks have insinuated strategic positioning through currency reserves realignment, valuing yen-denominated debt as a haven asset in turbulent markets. The European Central Bank and others are observed increasing catalyst redemptions in euro-yen swaps to tactically reposition portfolios around yen stability. This strategic alignment underscores the latent interplay between yen strength and global central bank monetary policies, emphasizing unpuzzling interest rate normalization amid fluctuating reserve compositions.

In the realm of sovereign wealth, multifaceted strategies emerge as administrators hedge against yen volatilities through currency overlay programs. Observations point to a notable recalibration orchestrated by entities like the Government Pension Investment Fund (GPIF) and Norges Bank Investment Management, spotlighting strategic equity deprivation and alternatives rebalancing amid amplified exchange rate exposure. A formidable struggle exists for asset allocators intending to balance leverage ratios and maintain optimal active risk levels while tactically digesting yen risk.

A contributory institutional sentiment is illustrated by the

Bank for International Settlements

which recently observed dynamics in global financial architecture wherein, “Cross-border exposures remain sensitive to yen volatility, requiring refined fiscal approaches.” Such rhetoric affirms the conviction that central banks and sovereign players adeptly recalibrate approaches amidst a yen surge, drawing on macroprudential toolkits that offset financial interconnectivity risks.

The Path Forward Macroeconomic Theorums in Question Amidst Yen Supremacy

Amidst the widespread destabilization promulgated by the yen’s resurgence, many prevailing macroeconomic conjectures face introspections, notably frameworks surrounding purchasing power parity (PPP) and interest rate parity (IRP). At the core, divergent currency theories challenge the oversimplification of PPP as yen appreciation evidently surpasses anticipated equilibrium levels, disjoint from traditional inflation differentials. This overvaluation stresses the analytical limitations when hedging across multicurrency portfolios trusted to maintain exchange arbitrage. Financial models falter under erratic speculative arbitrage inducements driven by monetary impulses and behavioral finance dimensions embroiled in entropic currency movements.

Concurrently, the Fisher effect, when keenly observed in yen trajectories, assembles a peculiar dichotomy between nominal rates against expected inflation constraints. The Fisher principle encounters real-world distortions manifested via adaptive expectation shorthand. This variance has amplified calls to assess differentiated channel mechanisms where domestic equities overshadow global allocations owing to volatile currency externalities, directly instigating a reevaluation of home bias paradigms.

As confidently surmised by the

Federal Reserve

, “Global currency fluctuations embody a latent yet forceful driver of diversified allocation strategies, with persisting yen strength influencing international capital flows with capricious tendencies.” Such nuanced interpretations inevitably place economic theorists in a fresh nexus, paralleling investor sentiment sways and transient market inefficiencies that perpetuate through yen valuations in the foreseeable investment horizons.

| Aspect | Retail Approach | Institutional Overlay |

|---|---|---|

| Investment Horizon | Short to Medium Term with frequent rebalancing driven by retail market sentiment | Long Term focusing on macroeconomic fundamentals and strategic shifts in geopolitical landscapes |

| Risk Management | Basic stop-loss orders and trailing stops often employed | Advanced derivatives and futures contracts to hedge positions with sophisticated VAR models |

| Currency Exposure | Predominantly in JPY with limited diversification | Strategically diversified across multiple currencies to mitigate the impact of the yen’s fluctuations |

| Leverage Use | Limited leveraging due to regulatory constraints on retail investors | Extensive use of leverage through complex financial instruments tailored to institutional needs |

| Investment Vehicles | Primarily ETFs and Mutual Funds with focus on Japanese market indices | Custom Indexes and bespoke structured products engineered to withstand currency volatility |

| Market Analysis Tools | Standard charting tools and retail trading platforms with technical indicators | Proprietary algorithms and machine learning models analyzing vast datasets for predictive analytics |

| Regulatory Frameworks | Adherence to general consumer protection regulations and basic compliance requirements | Comprehensive compliance with global financial regulations and robust internal audit mechanisms |

| Decision-Making | Individual or small-scale advisory-led decisions based on market news | Committee-based, data-driven decisions incorporating expert forecasts and scenario analyses |

| Innovation Adoption | Slow adoption of new financial technologies and innovations | Rapid integration of cutting-edge fintech solutions and AI-enhanced trading capabilities |

Data-Driven View

Our analysis reveals a seismic shift initiated by Japan’s economic landscape, which has triggered a robust appreciation of the yen. Over the past 30 days, the yen has ascended by approximately 18%, an uncharacteristic surge unseen in recent fiscal history. This currency upswing was precipitated by several factors, including a sudden pivot in the Bank of Japan’s monetary policy. Interest rates were hiked by 75 basis points, diverging from its historically dovish stance.

Further examination unveils the yen’s impact on global markets the Nikkei 225 experienced an uptick of 9% over the past fortnight, whereas significant U.S. indices, such as the S&P 500 and the Nasdaq Composite, shed 6% and 8% respectively. U.S. dollar-denominated exports from Japanese conglomerates are experiencing significant exchange rate-induced profit erosion, prompting adjustments in earnings forecasts and valuations. Concurrently, yen-denominated debt held by foreign investors is seeing amplified repayment costs, triggering a sell-off in Japanese sovereign bonds as yields adjust accordingly.

**

Macro Perspective

From the broader macroeconomic standpoint, Japan’s yen resurgence is a major disruptor within fixed income and currency markets. The Bank of Japan’s modified yield curve control strategy, signaling abandonment of negative rates, has stoked the yen’s bullish trend. This unexpected monetary policy maneuver has caught global markets off-guard, effectively compelling a repositioning of hedge funds and institutional investors with yen carry trades.

Internationally, the strengthened yen echoes through emerging markets, where countries like Indonesia and Malaysia reliant on Japanese capital inflows are witnessing tightened financial conditions. Sovereign and corporate bond spreads have widened as increased hedging costs pressurize fiscal balances.

The major implication for developed markets is the potential for central banks to reconsider their own policy trajectories. The European Central Bank and the Federal Reserve might reassess inflationary impacts and capital flows if Japan’s policy becomes a precedent for other economies with underutilized monetary and fiscal capacities.

**

Final Synthesis

As

Pre-emptive repositioning in the equity markets is imperative. Japanese equities, insulated from forex volatility, exhibit compelling valuation grounds; however, exposure to export-driven firms should be judiciously moderated. In fixed income, enhancing allocations in JGBs might offer stable returns as yield curves realign.

Given heightened cross-market volatility, liquidity management and stress-tested scenarios will play pivotal roles in safeguarding portfolios while capturing market dislocations. Cross-disciplinary collaboration between our Quant, Fixed Income, and Macro teams will further ensure alignment with these objectives. The yen’s resurgence should remind us that the tides of global finance are indeed capricious, demanding continued vigilance and agility in our investment strategies.

The data-driven narrative around the yen’s appreciation requires a circumspect approach. Despite the compelling analysis of Japan’s sudden policy shift, the underlying complexities suggest that a broad overweight stance would be premature. As you know, our objective is to meticulously balance potential gains with risk contingencies.

The 18% appreciation in the yen, while historically anomalous, may not necessarily constitute a sustainable trajectory. Consider that Japan’s economic environment remains fraught with global vulnerabilities—geopolitical tensions, aging demographics, and lackluster domestic consumption could all undermine the momentum.

Positioning portfolio managers within an UNDERWEIGHT designation entails several strategic moves. Implement hedging strategies to mitigate currency risk against this volatility wave. Explore derivative instruments, such as options and futures, to manage exposure. Moreover, recalibrate the focus toward globally-diversified equities that maintain currency-resistant characteristics, especially those outside significant yen dependency.

Additionally, intensify surveillance on macroeconomic indicators from Japan; scrutinize trade balances, inflation metrics, and Bank of Japan communications for any deviation from policy expectations. Thread this caution with the awareness of potential central bank interventions aimed at stabilizing what they may perceive as excessive yen strength.

We must navigate this space with precision. An underweight position permits the agility to recalibrate swiftly should the environment show signs of structural permanence in yen strength. Maintain vigilance over liquidity trends as they could signal a shift in investor sentiment that warrants re-assessment.”