- A significant portion of commercial real estate loans are set to mature, creating a refinancing challenge known as the ‘CRE refinancing cliff’.

- Regional banks, holding a substantial share of these loans, face heightened exposure and potential liquidity stress.

- Increasing interest rates exacerbate refinancing difficulties, driving potential defaults and reduced property valuations.

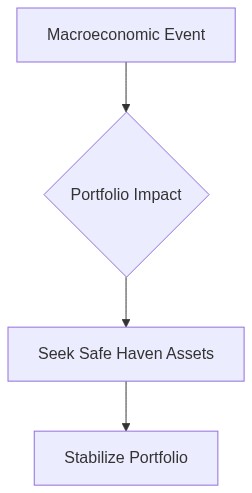

- Investors are increasingly viewing CRE exposure as risky, pivoting to safer assets in anticipation of destabilization.

- Regulators and policymakers are under pressure to mitigate systemic risks as the CRE market shifts.

“The market is a mechanism for transferring wealth from the impatient to the prepared.”

The Impending CRE Refinancing Apocalypse

Interest Rate Convexity and the Burden of Maturing Debt

As we dissect the current climate surrounding commercial real estate (CRE) refinancing, the profound implications of interest rate convexity take center stage. Over recent years, the Federal Reserve’s aggressive rate-hiking cycle has drastically altered the landscape for maturing CRE debt. Many loans, initially originated in the low-interest environment post-2008 financial crisis, are now confronted with refinancing at significantly higher yields. This has introduced substantial interest rate convexity challenges, meaning the sensitivity of borrowers’ potential refinancing costs to interest rate changes is becoming more pronounced. The liquidity premium demanded by investors to take on these newer, riskier loans is increasing, exacerbating the cost burden for CRE owners.

In light of the potential refinancing apocalypse, it is imperative to consider the price adjustments in the yield curve and their impact on debt servicingability. The CRE market often relies on predictable cash flows to service debt, and an unanticipated steepening of the yield curve intensifies debt service costs and reduces net operating income margins. This aspect is particularly critical given the large volume of CRE maturities expected over the next 18 to 24 months. Many borrowers, facing a convexity trap, will observe that the marginal increase in refinancing rates will lead to exponential increases in debt-servicing costs, threatening asset stability and market liquidity.

Moreover, as articulated by the Bank for International Settlements, “refinancing risks are amplified when a substantial portion of outstanding debt is short-term and stationary, susceptible to renewal under less favorable conditions.” This dynamic is particularly pressing against the backdrop of prevailing geopolitical uncertainties and volatile commodity prices, which further fuel inflationary pressures. As a result, CRE borrowers are becoming increasingly risk-averse, prompting a scramble to lock in refinancing deals sooner rather than later, potentially leading to a surge in demand that could skew market dynamics.

The Dichotomy of Asset Demand: Core vs. Secondary Markets

The CRE refinancing storm engenders a significant dichotomy between core and secondary markets. Investors, in a flight to quality, increasingly favor core markets which offer robust economic underpinnings and higher tenant demand, bolstering long-term asset valuations. This preference leads to tighter spreads in these markets, reflecting reduced default risk and a lower liquidity premium. Assets located in tier-one cities benefit from enhanced capital inflows, as investors perceive these markets as safer harbors amidst macroeconomic turbulence. The resilience of these markets is further underscored by their ability to adapt to evolving demographic trends, such as urbanization and shifts towards remote working ecosystems.

Conversely, secondary markets face dichotomous risks as liquidity erodes in the face of uncertain market outlooks. These markets, characterized by less economic diversification, are increasingly vulnerable to external shocks and the aforementioned convexity risks. As capital retreats, valuations in secondary markets face downward pressure, creating a feedback loop where refinancing becomes untenable, thus prone to heightened default probabilities. Such scenarios are evident in over-levered assets within markets traditionally pivotal to CRE portfolios but now face the specter of subdued demand and potential capital flight.

The Federal Reserve has noted that, “while credit conditions remain stable at large, differentiations in market risk are increasingly scrutinized as economic conditions diverge significantly across regions.” This divergence implies that a one-size-fits-all approach to managing refinancing risk is impractical, demanding bespoke strategies for portfolio diversification and risk mitigation. Fund managers must prudently evaluate asset pricing against market-specific benchmarks, ensuring that return profiles adequately compensate for the heightened risk.

The Role of Structured Finance and Securitization Complexity

The structured finance and securitization markets wield significant influence over the impending refinancing challenges plaguing the CRE sector. As commercial mortgage-backed securities (CMBS) and collateralized debt obligations (CDOs) mature, the inherent complexities in these products call for meticulous scrutiny. Securitization structures have enabled the redistribution of risk; however, they also introduce opacity, imperiling certainty regarding underlying asset performance. The disintermediation of traditional banking in favor of shadow banking has exacerbated vulnerabilities, complicating refinancing pathways for CRE investors within structured tranches.

An examination into the maturity profiles of CMBS reveals burgeoning risks associated with potential maturity defaults, particularly where tranches are backed by underperforming real estate assets or situated in distressed market geographies. The structured nature of these financial products means asset repricing within tranches can induce spillover effects, leading to significant valuation adjustments and repricing of risk within the broader CRE market. The intricacies of adjusting these portfolios in market conditions subject to significant rate volatility only add to the complexity, highlighting the critical need for adept portfolio management strategies.

Furthermore, the regulatory environment governing securitizations could further impact refinancing dynamics. In this regard, the Bank for International Settlements underscores, “the necessity to ensure comprehensive regulatory frameworks support both financial stability and market transparency, especially when confronting latent systemic risks in structured products.” The interplay between regulatory adjustments and market sentiment introduces an additional layer of uncertainty, challenging fund managers to meticulously align risk management practices with evolving legal standards and market conditions.

| Criteria | Retail Approach | Institutional Overlay |

|---|---|---|

| Target Audience | Individual Investors | Institutional Investors |

| Investment Size | Small to Medium | Large Scale |

| Risk Management | Basic Diversification | Advanced Hedging Techniques |

| Market Analysis | General Trends | In-depth Quantitative Models |

| Access to Information | Publicly Available Data | Proprietary Research and Data |

| Regulatory Compliance | Standard Retail Guidelines | Strict Institutional Protocols |

| Fee Structure | Commission-Based | Performance-Based Fees |

| Liquidity Requirements | Higher Liquidity Needs | Lower Liquidity Needs |

| Technology Use | Online Platforms | Advanced Analytics Tools |

| Decision Making Process | Individual Decisions | Collaborative Institutional Decisions |

1 thought on “**The Impending CRE Refinancing Apocalypse**”